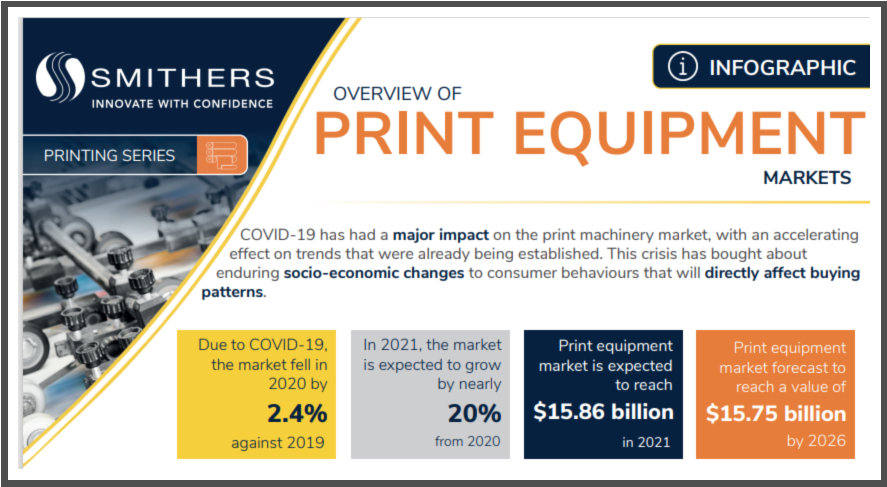

Data from the new Smithers report – The Future of Print Equipment to 2026 – show that the value of global sales of printing and finishing equipment fell from $17.3 billion in 2019 to $13.2 billion in 2020. It is expected to rebound to $15.9 billion in 2021.

Smithers’ expert forecasting finds that sales value will struggle to recover to this pre-pandemic level after

this initial rebound in 2021. Their analysts believe the market for printing and finishing equipment will be essentially flat, with a -0.2% compound annual growth rate (CAGR) for 2021-2026 at constant prices.

This challenging outlook will place a premium on new technologies, value-adding systems and services plus greater automation as print-equipment manufacturers seek to maintain profitability.

Geographic and Segment Differences

From 2021-2026 the largest growth market for equipment sales will be in Asia, especially

India and China.

Demand will decline in both Western and Eastern Europe.

North and Latin America will also see moderate rises in equipment sales by value over the period, of close to 1.0% CAGR.

The seismic impact of 2020 is being felt in all printing and finishing technology sectors and geographic markets, but not equally. Smithers’ analysis shows that a few segments will continue to expand through the 2020s as the buyers and print service suppliers adjust to a business environment reshaped by the experience of the pandemic.

The most severe effect will be in sales of analog platforms used in commercial print and publications, with some smaller print service providers pushed out of business. These applications were already in decline with falling print volumes across the 2010s. Now exacerbated by Covid. Smithers forecasts a -1.9% decline year-to-year for analog equipment over the next 5 years.

Overall increased demand for packaging presses and digital technology will largely balance out

this decline in demand for analog publishing presses, however.

Across the Smithers forecast period, the installed base of digital presses will grow overall, with electrophotographic presses adding particularly to the installed base.

The installed base of inkjet presses is forecast to be essentially static between 2021 and 2026, as the removal of wide-format presses compensates for greater use of single-pass and sheet-fed units in packaging and other alternative applications.

A leading trend that has seen a marked acceleration in 2020 is the shift to shorter print runs,

which is shifting the per unit print costs in favor of digital (inkjet and electrophotography)

presses.

Digital equipment is easier to integrate with e-commerce, web-to-print and print-on-demand service models, which are increasingly popular. Digital equipment can also deliver value-adding variable

data print.

In the short-term. many technology leaders are more focused on incremental improvements to existing platforms, until revenues recover. Tighter budgets mean there will also be more pressure on printing equipment manufacturers to revise their ink pricing strategies.

Traditional analog press builders are innovating in this space. Automation in prepress, on-press plate making and automated wash up will be priorities for analog press manufacturers to boost

operational effectiveness and maintain margins and profitability.

The cancellation of drupa 2020, and a reduced attendance at virtual drupa 2021, has broken

the industry’s reliance on this key event in the print calendar. This is leading firms to

investigate new online sales and marketing channels to engage with a global customer base

and demonstrate their latest equipment.

This matches with the imperative to offer more direct remote service and support online as Covid restricted on-site visits. Direct remote service and more online support will remain highly effective and low-cost means for both problem-solving and preventive maintenance, with conventional technology now supplemented by mobile and augmented reality systems.

About the Report

The Smithers “Future of Print Equipment Markets to 2026” report looks at the growth of the print equipment market across all key segments and geographic regions. It also examines the downturn in 2020 and reviews the extent and rate of recovery.

The focus of this report is on the print equipment used for commercial, packaging and production printing by print service providers (PSPs) and by packaging converters.

This report is based on extensive primary and secondary research. Primary research consisted of targeted interviews with printing material suppliers, converters and experts from key markets. This was supported by secondary research in the form of extensive literature analysis of published data, official government statistics, domestic and international trade organization data, company websites, industry reports, trade press articles, presentations, and attendance at trade events.

The primary author is Jon Harper Smith. His 15+ years of printing industry experience includes working with Fujifilm and industrial and package-printing businesses.

For more information about the Smithers report and the types of charts it contains, visit: https://www.smithers.com/services/market-reports/printing/future-of-print-equipment-markets-to-2026

For more information about Smithers, visit: https://www.smithers.com/about-us